Red Flags When Hiring a Bank Risk Executive

Banks usually don’t mis-hire a risk executive because the candidate looked obviously reckless, unserious, or unqualified. The more common mistake is subtler. The candidate interviews well, uses all the right language about enterprise risk and strategic partnership, and leaves the room sounding credible. The problem is that the hiring process often rewards polished behaviors before it tests judgment. In banking, that’s a serious failure.

The Federal Reserve’s guidance on board effectiveness makes clear that boards are expected to set direction on strategy and risk appetite, define the information they need, hold senior management accountable, and support the independence and stature of independent risk management.

That makes this role different from a generic senior leadership hire. A bank risk executive is not just supposed to be thoughtful, experienced, and commercially aware. The job sits inside a governance structure. The OCC’s Heightened Standards in Appendix D to 12 CFR Part 30 expect a formal risk governance framework, unrestricted access for the chief risk executive to the board, and supporting talent development and succession practices for roles that influence material risk decisions.

So, the biggest red flags are often not personal flaws in the candidate. They are flaws in how the bank defines, interviews for, and evaluates the job.

Table of Contents

Why Banks Keep Missing the Real Warning Signs

Banks often approach this search as if they’re hiring a broad executive profile instead of a governance-critical role. They say they want leadership, maturity, communication skills, and business judgment. None of that is wrong, but it is too general for the situation.

If the hiring process is only focused on these traits, the search starts favoring candidates who are smooth, familiar, and easy to imagine in the role, rather than candidates who have proved they can challenge line management, escalate uncomfortable issues, and operate credibly with the board.

The scope of bank risk leadership has also expanded, giving banks an even stronger reason to ensure they focus on the right things when hiring these positions. The EY/IIF Global Bank Risk Management Survey found that the CRO role continues to broaden, cyber risk remained the top near-term priority, and banks increasingly wanted critical thinking, analytical strength, and organizational agility from risk leaders.

A weak hiring process misses the real warning signs because it asks the wrong questions. It treats executive confidence as a proxy for governance judgment. It treats commercial fluency as a proxy for independence. It treats broad experience as a proxy for current-state readiness. Those shortcuts are exactly how a bank ends up with someone who looks right on paper and sounds right in an interview but is still wrong for the institution.

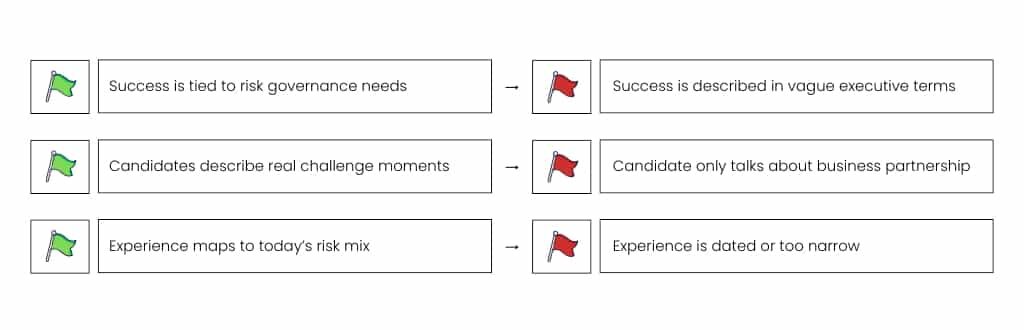

Red Flag #1: The Hiring Committee Cannot Clearly Define What Success in the Role Looks Like

One of the first warning signs often appears before the candidate says a word. The bank itself is not clear on what it needs.

Some searches begin with a vague mandate: hire a strong risk leader, someone strategic, someone who can partner with the business, someone who can help the board. That sounds sensible until it becomes obvious that nobody has translated those ideas into operating expectations. Does the bank need someone to tighten governance after a period of growth? Someone to professionalize an underbuilt second line? Someone with stronger board-facing discipline? Someone who can manage a more complex mix of fraud, cyber, operational, and credit risk? Those are all very different jobs.

When the role definition stays fuzzy, interviews get fuzzy too. Candidates are rewarded for giving high-level answers because the bank hasn’t anchored the search to specific deliverables, reporting demands, escalation expectations, or team-building requirements. That creates a false sense of alignment. The candidate sounds right because the bank never forced the discussion into specifics.

This is where regulatory guidance is more useful than generic executive-search language. The Federal Reserve’s board guidance and the OCC’s Heightened Standards are concrete about what a mature governance structure is supposed to support: risk appetite oversight, management accountability, information flow to the board, independent risk management, and formal governance architecture. If a bank can’t define where the executive fits inside that structure, it’s not really ready to evaluate the hire.

Red Flag #2: The Interview Rewards Polished Language Instead of Proof of Risk Governance Judgment

Risk candidates usually know how to talk. They can speak fluently about culture, challenge, resilience, alignment, strategic partnership, transformation, and enterprise-wide thinking. The problem is that many interview processes stop there. They reward the candidate for sounding like a senior executive without requiring evidence that the person has made difficult governance decisions in live situations.

In this role, real judgment shows up when growth goals and risk discipline collide. It shows up when the candidate has to explain a board reporting change, describe a formal disagreement with a revenue leader, defend an escalation, or walk through how a risk appetite breach was identified and handled. Those moments tell a bank far more than a polished answer about leadership style ever will.

A surprising number of interviews never get close to that level. The candidate says they have worked cross-functionally. Fine. They say they value independent challenge. Fine. They say they are comfortable with boards. Fine.

But none of those statements are enough on their own. A bank should want proof: what issue, what conflict, what decision, what outcome, what lesson, what change in process followed?

The real red flag here is unsupported fluency. A candidate who sounds strategic but can’t point to specific governance actions is often being rewarded for performance in the interview, not performance in the job.

Red Flag #3: The Bank Says It Wants Independence, But Interviews For “Business Partnership”

Banks want risk executives who understand the business. That part is reasonable. A risk leader who can’t communicate with lending, operations, finance, technology, and senior management will struggle. But many banks take that idea too far and end up hiring for commercial comfort instead of credible independence.

This happens when the interview process quietly favors the candidate who seems least likely to create tension. The hiring committee says it wants collaboration. The candidate responds by emphasizing relationship-building, support for growth, and being solutions-oriented. Again, none of that is inherently wrong. The problem is what gets left out. Independent risk management is supposed to challenge line management when needed. It is supposed to surface disagreement, not absorb it quietly.

The Federal Reserve’s guidance stresses the importance of the independence and stature of independent risk management, and the OCC’s Heightened Standards require unrestricted access for the chief risk executive to the board or relevant committees. Those expectations only matter if the person in the role is willing and able to use that independence when it counts.

A bank can therefore create its own red flag by interviewing as though the right candidate should feel effortless to the business. In reality, a strong risk executive should be able to work with line leaders without being captured by them. If the candidate only describes harmony, the bank should worry. If the interview never tests how the candidate handles pushback, the bank should worry even more.

Red Flag #4: The Interview Process Does Not Test for Current Risk Complexity

Another common problem is that banks still assess the role as though the risk environment hasn’t changed in years. They still place heavy weight on traditional bank tenure and assume that is enough. It often is not.

The risk mix has widened. Fraud pressure is up, AI-enabled scams are now a live concern, cyber and operational resilience remain central issues and third-party dependency is harder to ignore. Even where credit, liquidity, and balance-sheet oversight remain core, they no longer define the role by themselves.

The FDIC’s 2025 Risk Review points to continuing pressure across net interest margins, funding and liquidity, commercial real estate, leveraged lending, private credit exposure, and consumer credit categories. Bank Director’s 2026 Risk Survey found that 79% of bank leaders ranked fraud as a top risk, with 84% especially concerned about AI-related fraud and scams targeting customers and 77% concerned about threats targeting employees and the organization.

That makes one kind of candidate especially misleading. The person may have strong credentials and years inside banking, but most of their operating experience may reflect a narrower and older risk agenda. A bank can mistake that familiarity for readiness when in reality, the candidate has very few skills that relate to the modern-day banking risks.

You’re not necessarily looking for a candidate with deep banking experience; you’re looking for experience that maps to the bank’s current and future risk reality. If the hiring process doesn’t test that directly, it leaves a major red flag untouched.

Red Flag #5: The Bank Never Pressure-Tests How the Candidate Handles Board Communication

A bank risk executive exists in part because the board needs clear, credible, decision-useful information about the institution’s risk profile, risk appetite, emerging exposures, and management’s response. The Federal Reserve’s board guidance is explicit that boards should direct management on the information they need to oversee the firm’s activities and to hold senior management accountable.

That means a bank should not be satisfied with a candidate who merely seems articulate in a conference room. The real question is whether the person can brief directors when the facts are incomplete, the issue is politically sensitive, and the implications cut across several parts of the institution. Can they explain what changed, why it matters, what management is doing, what remains uncertain, and where board attention is needed? Can they do that without minimizing the issue or drowning it in jargon?

Many interviews never test this. They ask whether the candidate has presented to boards before. The candidate says yes and that answer is taken as enough even though there’s nothing to back it up.

The bank should want to see how the person frames ambiguity, escalation, prioritization, and residual risk in front of directors. Otherwise, it’s assuming one of the role’s most important capabilities instead of evaluating it.

Red Flag #6: The Process Focuses on the Individual and Ignores Whether They Can Build a Real Risk Bench

Many hiring committees become absorbed in whether the senior executive seems strong enough individually but fail to ask whether the person can leave behind a stronger second line than the one they inherited.

One capable individual doesn’t create safety alone. Banks become safer when the function beneath that executive gets more disciplined, more capable, and more durable. A risk leader who centralizes expertise in themselves can look impressive in the short term but the longer-term result is a fragile organization where too much judgment routes through one person and too little capability sits in the next layer down.

Bank Director’s 2025 Compensation & Talent Survey found that 30% of bank leaders either lacked an effective long-term succession plan for key C-suite executives beyond the CEO or had no such plan at all. That matters because risk leadership is precisely the kind of function where weak succession and shallow bench strength create governance vulnerability.

The executive you’re looking for should be capable of creating a team that can support the work that needs to be done and creating a succession plan that won’t leave the bank in a vulnerable position. A bank that never evaluates team building, manager development, and second-line architecture is not fully evaluating the hire.

A Strong Bank Risk Executive Should Leave Behind More Capability Than They Inherited

The right executive should make the risk function more durable. That means clearer ownership, better manager depth, more disciplined reporting, more consistent escalation standards, and more visible succession beneath the top role. A strong risk leader should reduce key-person dependence over time, not deepen it.

That expectation isn’t separate from governance either. The OCC’s Heightened Standards explicitly tie the safety and soundness of a bank’s risk governance framework to compensation, performance management, talent development, recruitment, and succession planning for people whose roles influence risk outcomes.

This is where a hiring process should become more demanding. It should ask what kind of team the candidate inherited, what they changed, how they developed managers, how they improved reporting discipline, where they built talent pipelines, and what the bench looked like when they left. Without that lens, a bank may hire a strong operator who never becomes a real builder.

One Hiring Mistake Smaller Banks Make More Often Than Larger Institutions

Community and mid-sized banks often need a different hiring filter than very large institutions, and this is where many of them drift into avoidable mistakes.

Smaller institutions often tell themselves they need someone flexible, practical, and able to wear many hats. While that’s understandable, the risk is that flexibility becomes a substitute for structure. The bank hires a broadly experienced executive who fits the culture and can function in a lightly built environment, but they don’t actually know how to formalize governance, sharpen board reporting, or build stronger second-line processes.

Larger institutions can make the opposite mistake. They may overweight pedigree, large-bank title history, and institutional prestige. That can produce a hire with the right background markers but the wrong level of adaptability or practical influence.

Bank Director’s 2025 Compensation & Talent Survey is especially applicable here because its respondent base was drawn from U.S. banks under $100 billion in assets, where succession gaps and talent architecture remain active concerns. The implication isn’t that smaller banks need a lighter version of a chief risk officer, but they do need the right version for their size, complexity, and board maturity. Hiring for general executive fit instead of that institutional fit is its own red flag.

Questions That Expose These Red Flags Before the Hire

A stronger process asks harder questions of candidates.

Instead of asking broad prompts about leadership style, a bank should force the candidate into the real operating tensions of the role. Questions like these are more revealing:

- Tell us about a time you formally disagreed with a revenue leader on a material risk issue. What happened, and how was it resolved?

- What information should a board receive monthly or quarterly from the risk function, and how would you decide what deserves director attention?

- Describe a risk appetite breach or limit issue you managed. How was it identified, escalated, communicated, and closed out?

- Where have you had direct influence over staffing, succession, and capability-building in the risk function? What changed because of your leadership?

- Which emerging risks do you think banks still underweight, and what would you change in the first year here?

- How do you distinguish being commercially informed from being commercially captured?

- What support would you need from the CEO and board to maintain appropriate independence in this role?

Questions like these do more than test fluency; they test judgment, escalation discipline, board communication, independence, and team building. That’s what the bank actually needs to know.

What Banks Should Look for Instead

The bank should be looking for evidence.

It should look for someone who can explain real governance decisions in concrete terms. Someone who has challenged management without losing credibility. Someone who can speak to the board in plain language without flattening uncertainty. Someone whose experience fits the institution’s current risk mix, not just its traditional categories. Someone who has built a stronger team beneath them, not merely performed as a strong individual. Someone who understands that independence is not hostility, but it is also not passive agreement.

That standard is much closer to what regulators expect from a mature governance structure. The Federal Reserve’s guidance and the OCC’s Heightened Standards both point toward a model in which risk appetite, information flow, accountability, independent challenge, and functional durability matter more than executive theater.

A bank that hires against those criteria is less likely to be seduced by the wrong signals.

Final Takeaway

The most dangerous bank risk hires are not always the ones with the most obvious flaws. They’re often the ones selected through a process that mistakes polished interviewing for governance readiness.

That is why the biggest red flags often start inside the hiring committee. The bank is too vague about the role. It interviews for business comfort instead of independent judgment. It rewards broad language instead of concrete evidence. It checks for experience without testing for current risk complexity. It evaluates the executive personally without asking whether they can build the next layer of risk leadership beneath them.

In bank risk hiring, the interview process is often the first real control test.

For help improving your interviewing and hiring process, talk to the banking recruitment experts at The Richmond Group USA. With years of experience in the industry, we know what we’re looking for and how to find it. Get started with us today!

Frequently Asked Questions About Hiring a Bank Risk Executive

What Are the Biggest Red Flags When Hiring a Bank Risk Executive?

The biggest red flags are usually not superficial personality issues. They’re signs that the candidate may not function well inside the bank’s real governance structure. That includes weak evidence of independent challenge, vague answers about board communication, narrow experience that doesn’t match today’s risk mix, and little proof that the person can build a durable risk bench beneath them.

What Should Boards Look for in a Chief Risk Officer?

Boards should look for independent judgment, clear communication, credible escalation discipline, comfort with current banking risk complexity, and evidence that the candidate can strengthen the broader function rather than simply perform as a strong individual. The Federal Reserve and OCC both reinforce the importance of risk appetite oversight, management accountability, independent risk management, and strong governance architecture.

How Do Banks Avoid Hiring the Wrong Chief Risk Officer?

Banks reduce hiring risk by defining the role clearly before the search begins, structuring interviews around real governance scenarios, testing how the candidate handles board reporting and disagreement with the business, and evaluating whether the candidate can build a stronger risk team beneath them.

Should Smaller Banks Use the Same CRO Hiring Criteria as Larger Banks?

Not exactly. The core governance principles are similar, but the right executive profile depends on the bank’s size, complexity, and maturity. Smaller institutions often need someone who can build structure and sharpen governance discipline, while larger institutions may place more weight on navigating complexity across a broader enterprise.