AI In Accounting Isn’t Replacing Accountants. It’s Changing the Skills Finance Teams Need

Finance teams keep getting asked to do more with the same headcount. Close faster. Explain variance in plain English. Build forecasts that survive contact with reality. Answer investor questions. Support pricing, headcount planning, and capital allocation.

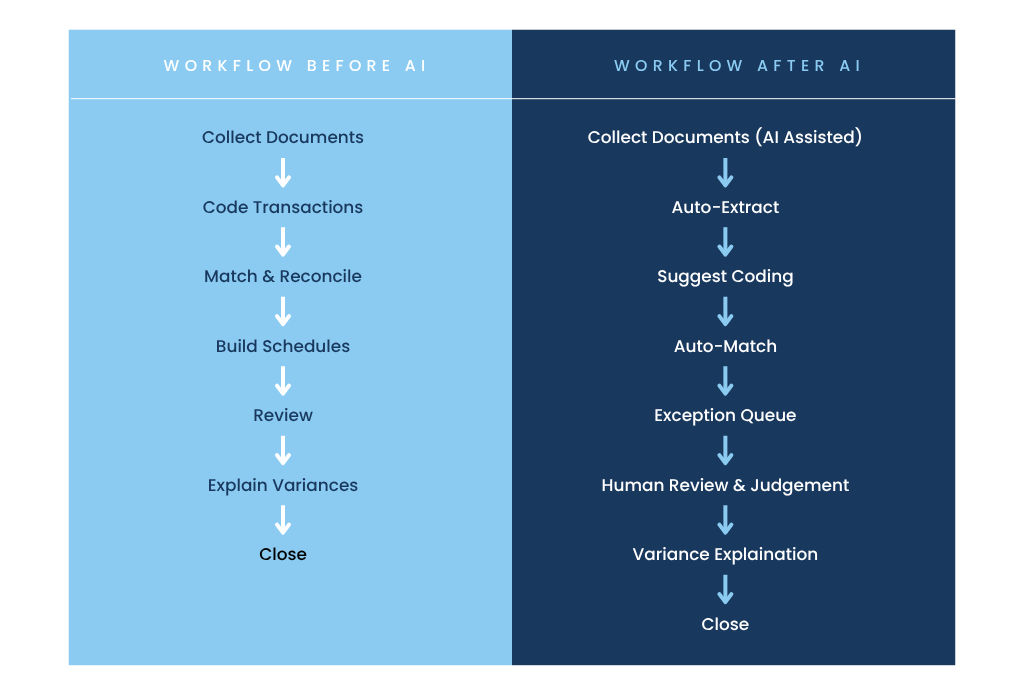

At the same time, the work that used to soak up a big share of accounting hours is getting automated. Transaction coding, document extraction, matching, and reconciliation increasingly happen inside the tools. Less “enter and check,” more “review and interpret.”

That shift triggers the question accountants keep hearing, sometimes from leadership and sometimes from their own teams.

Will AI replace accountants?

The short answer is no. While many of the entry level tasks accountants used to perform are now being performed by AI, the data produced by AI still needs to be reviewed and interpreted by a human.

The real issue now is the mismatch of skills that AI is creating. Instead of just needing accounting skills to do the job, candidates now need a combination of IT and finance skills to fully benefit from the use of AI.

So, what does all this mean for the future of accounting? How do businesses adapt to these changes and reframe their roles to work with AI?

Table of Contents

Why AI In Accounting Is Advancing So Quickly

Accounting runs on structured information. Vendors, invoices, journal entries, ledgers, reconciliations, and audit trails follow repeatable patterns. These patterns make the role unusually compatible with automation.

Stanford’s overview of this research makes the point directly: accounting often is often listed among the most automatable work because of how much of it involves routine processing like data entry and reconciliation.

AI performs best when a task has three traits: lots of historical examples, consistent formats, and measurable “right answers.” Many accounting workflows fit that description.

What AI Is Actually Automating in Accounting

The most common AI impact in accounting is not “strategic finance.” It’s replacing the repetitive parts of the workstream and turning the accountant into a reviewer, investigator, and explainer.

These are the areas getting automated first:

Transaction Categorization and Coding

Systems learn from prior coding decisions and apply likely classifications to new activity. Humans still correct edge cases, but fewer transactions require manual handling.

Reconciliation and Matching

Tools match bank activity to ledger entries, flag exceptions, and route discrepancies for review.

Invoice and Receipt Extraction

Document AI pulls line items and terms into structured fields that flow into payables and expense systems.

Exception Detection

Models identify anomalies such as duplicate payments, outlier amounts, unusual vendors, or timing patterns that merit review.

A research paper focused on AI automation in routine accounting tasks describes the efficiency gains and the workforce implications, including the shift toward higher-skill responsibilities.

Evidence Shows AI Is Raising Output in Accounting Work

The Stanford/MIT field evidence on AI in accounting matters because it measures what actually happens inside firms, not what people speculate might happen.

The findings reported through Stanford and MIT include three practical outcomes:

- Higher throughput: AI adopters support 55% more clients per week.

- Time reallocation: about 8.5% of time moved away from routine processing.

- Faster close: close cycles shortened by about 7.5 days.

Those results imply a simple operational truth: when the machine does more of the first draft work, humans spend more time on review quality, client communication, and analysis.

AI Is Quietly Removing the First Step of the Accounting Career Ladder

Entry-level accounting jobs have historically been built around repetition. New staff learned the system by doing the work: coding transactions, preparing reconciliations, tracing support, building schedules, and working through exceptions until patterns became obvious.

AI compresses that learning cycle by shrinking the volume of work that forces repetition. The new accountant sees fewer raw transactions and fewer messy reconciliations, which can slow the development of judgment. The missing piece in many organizations is a plan for how juniors develop skills when they no longer have the repetitive tasks to help develop them.

If finance leaders ignore this, the risk won’t show up this quarter. It will show up in three to five years when your bench is thin and fewer people can handle ambiguity without escalation.

A controller can spot this early by looking at a basic metric: how often junior staff members touch exceptions versus how often they only review AI-suggested outputs. If the second number dominates, training debt is accumulating.

The Rise of the Accounting Analyst

As routine processing gets automated, a new type of role becomes valuable: someone who understands accounting mechanics and can also interpret system output, investigate drivers, and explain results to the business.

At The Richmond Group USA, we’ve noticed a recent increase in the need for “Accounting Analyst” roles. This term gets used loosely, so it helps to define it.

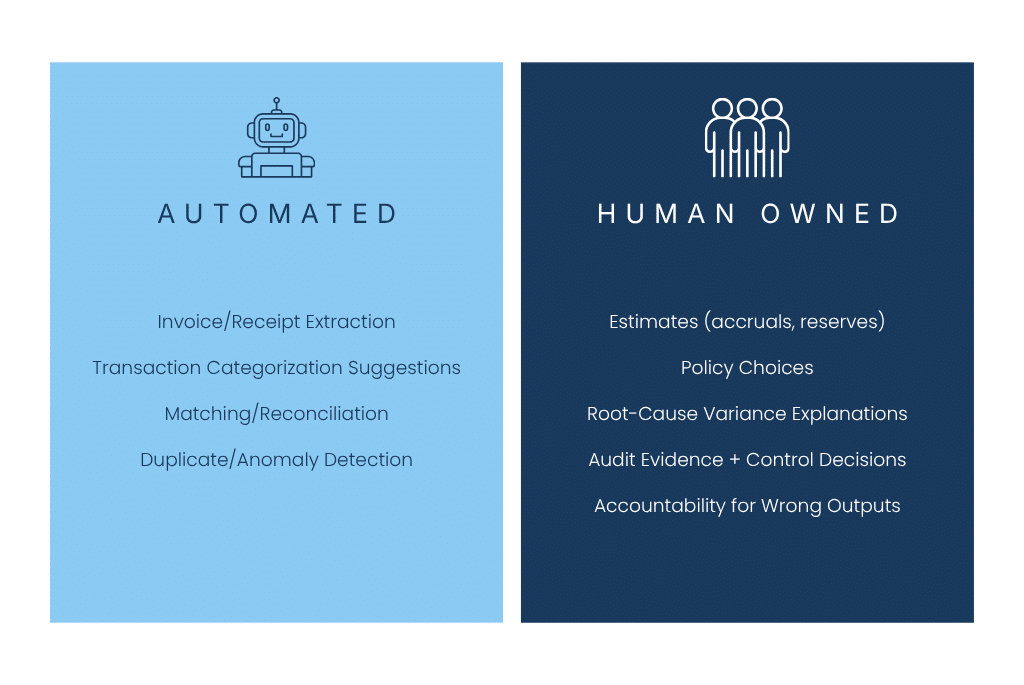

What An Accounting Analyst Typically Owns

- Variance investigation tied to the close, not only reporting

- Trend interpretation across ledger detail and operational signals

- Review of AI-driven suggestions and exception queues

- Building schedules that support judgment calls (accruals, reserves, allocations)

- Writing narrative explanations leadership can use

How This Differs from Nearby Roles

- Staff accountant: executes the close tasks and reconciliations, increasingly with automated first drafts.

- FP&A analyst: owns forecasting and planning models; uses accounting outputs as inputs.

- Finance systems analyst: owns tool configuration and data flow; often sits closer to IT.

The Accounting Analyst sits between accounting and decision support. The role exists because the organization needs someone to translate “system output” into “business meaning.”

MIT’s coverage of the Stanford/MIT findings highlights this shift toward analysis and client-facing work once AI handles routine tasks.

The Importance of Defining These Roles

While many businesses are now looking for these “Accounting Analyst” roles, most of them can’t clearly define what the role entails. They know that they need someone to interpret data but they aren’t sure how to define the actual responsibilities of the role.

Role ambiguity is consistently linked to higher intent to quit in organizational research, even when the rest of the work environment is controlled. A recent study found that role ambiguity contributes to employees’ intention to quit and increases emotional demands.

As the adoption of AI in accounting becomes more widespread, it’s important for leaders to define the requirements for these types of roles. If you can’t explain what you need, how do you expect to find the right person for the job?

The Skills Gap Emerging in the Accounting Profession

The skills gap is not about turning accountants into engineers. It’s about giving finance professionals enough analytic fluency to evaluate outputs, catch errors, and explain drivers.

Research analyzing accounting labor-market needs points to a growing mismatch between what employers ask for and what many training pathways deliver.

In practice, the highest-value skills cluster into a few buckets:

Analytical Skills That Now Matter More

- Root-cause analysis of variances

- Comfort with messy data and imperfect classifications

- Building and testing assumptions (not just recording outcomes)

- Communicating uncertainty

Tool Fluency That Actually Shows Up on the Job

- Working inside automated reconciliation and exception workflows

- Using BI tools to trace drivers (not just exporting to Excel)

- Understanding data lineage enough to diagnose a bad number

This is why some finance teams feel stuck. They buy automation tools and still end up with the same questions from leadership, except now the team must also explain what the model did.

Why Accounting Education Is Under Pressure to Evolve

Professional bodies have been signaling this shift for a while. IFAC’s work on preparing future-ready professionals focuses on digital transformation and the need for broader competencies across the profession.

The hardest part is that education systems are optimized for standardization. They teach rules that will be tested. AI pushes finance work toward judgment, interpretation, and cross-functional context, which are harder to grade and harder to teach at scale.

That gap leaves employers with a choice: build training internally or accept weaker capability growth.

Why Human Judgment Still Matters in Financial Decision Making

“Human judgment” can sound like a slogan. In accounting, it shows up in specific places.

- Revenue recognition edge cases

- Reserve and accrual estimates

- Materiality decisions

- Policy choices that require context, not pattern matching

- Audit evidence and control design

- Accountability when an automated suggestion is wrong

Research on human-AI collaboration in accounting emphasizes that professionals remain essential for interpreting outputs and evaluating outcomes in context.

This matters for CFOs and business owners because financial reporting carries accountability. Automation can improve speed and consistency, but responsibility stays human.

How Finance Teams Can Adapt Without Turning the Close into an Experiment

Teams that handle this transition well tend to do a few practical things early.

Define Roles and Ownership Clearly

If “Accounting Analyst” means three different things across departments, hiring and development breaks. Finance leaders benefit from writing role definitions that separate:

- Close execution

- Exception investigation

- Forecast support

- Systems ownership

Build A Real Training Path for Juniors

If AI removes volume reps, training must become intentional. Rotations through exception queues, variance review, and audit support create the pattern exposure juniors used to get from repetitive work.

Treat AI Output Like a First Draft, Not A Verdict

AI accelerates the first pass, humans own the final call. Teams should set review thresholds and escalation rules, especially around estimates and policy-sensitive areas.

What The Future of Accounting Looks Like

Accountants are not going to disappear, but the role will change. New responsibilities become less about producing numbers and more about explaining them.

AI keeps absorbing routine processing. Finance leaders keep asking for faster, clearer insights. The distance between those two creates a skills gap.

Accountants who build analytic fluency and interpretive strength become more valuable. Finance teams that redesign training and role boundaries avoid the quiet risk of a hollowed-out bench.

If you’re looking for talent that can handle these new expectations, let our team of expert accounting recruiters assist you. Our accounting recruiters have first-hand experience searching for and placing talent that can handle the new demands that AI has created. We’re confident that we can do the same for you and your team.

To start the conversation, contact us or reach out to our VP of Accounting & Finance Division, Krissy Whitaker.

Krissy Whitaker

VP of Accounting & Finance Division

(804) 404-2801 ext. 2801

krissyw@richgroupusa.com